Every founder wants to know the same thing: which tools are actually winning right now? Not which got the most venture funding or the best TechCrunch headline. Which ones are companies actually spending more on?

We analyzed spending growth across thousands of companies from Q1 2025 to Q1 2026. The results tell a story about how modern development teams, product teams, and knowledge workers are fundamentally reshaping their toolkits. Spoiler: AI isn't just winning. It's redefining categories.

The AI Acceleration Is Not Hype

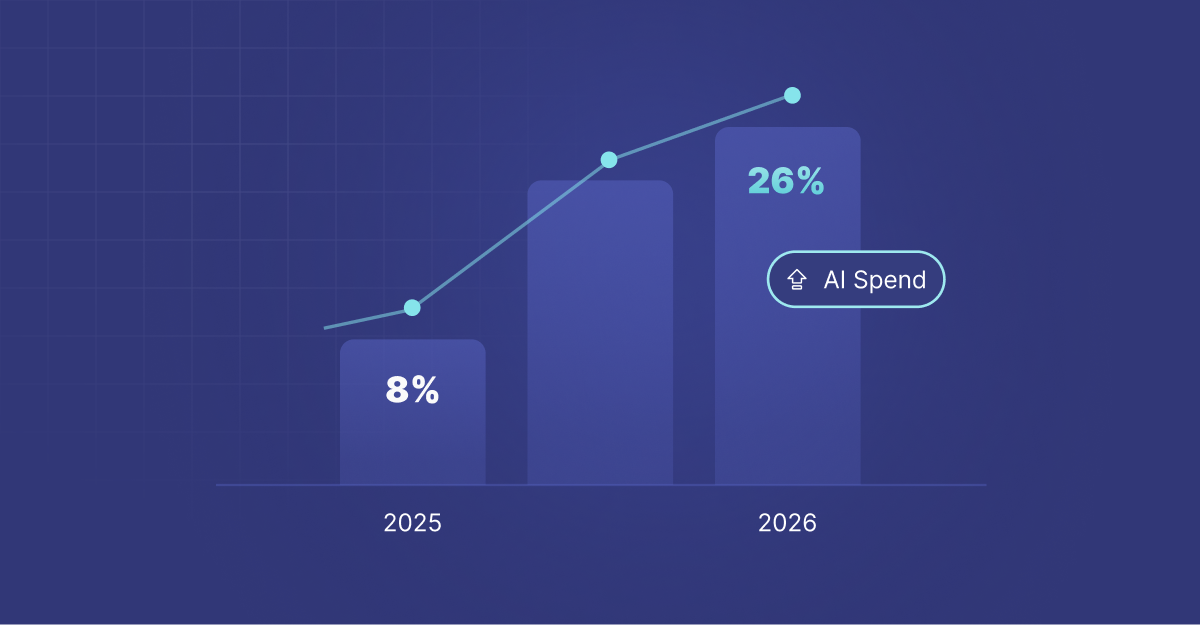

Before we dig into the specific winners, the macro trend: AI-related spending jumped from 8.8% of all SaaS transactions in January 2025 to 26.4% by March 2026. That's a 3x increase in market share in 14 months.

This isn't just LLM API calls spiking temporarily. This is companies integrating AI into core workflows. It's not a fad wave. It's a structural shift in how development and knowledge work happens.

With that context, let's look at the 15 fastest-growing tools.

The 15 Fastest-Growing Tools

1. Lovable (+2089%)

The explosive winner. Lovable is an AI code generation platform that turned simple prompts into full React applications. The growth rate suggests companies are using it heavily for rapid prototyping and internal tools. This isn't just developers experimenting. Teams are standardizing on it.

2. Claude (+1728%)

Anthropic's Claude AI model is growing faster than any traditional SaaS tool ever has. Companies are integrating it into customer service, content generation, code review, and research workflows. The API is becoming embedded infrastructure.

3. Anthropic (+1538%)

The parent company spend is growing nearly as fast as Claude itself. This reflects companies buying Claude Credits, using Claude through enterprise agreements, and exploring custom deployment options. Enterprise adoption is accelerating.

4. Firecrawl (+1417%)

A web scraping and data extraction tool built for AI workflows. Its explosive growth reflects the emerging category of AI data preparation. Companies need clean, structured data to feed into LLMs. Firecrawl is becoming essential glue.

5. OpenRouter (+1009%)

A router that lets developers access multiple LLM APIs through one interface. Its growth shows that teams want flexibility and aren't locking into a single model vendor. Companies are hedging their AI bets, which is smart.

6. n8n (+812%)

An open-source workflow automation platform. Its growth reflects a shift from Zapier toward more flexible, customizable automation. Companies want to own their workflows rather than rent them from a SaaS vendor.

7. Granola (+593%)

A meeting intelligence and note-taking tool. Growth suggests companies are finally solving the "someone summarize this Zoom call" problem at scale, not just with one power user.

8. Gamma (+531%)

An AI presentation generator. Fast growth here indicates that the slide deck itself is becoming automated. Why spend an hour on formatting when AI does it in seconds?

9. Langfuse (+455%)

An observability and analytics platform for LLM applications. As companies ship more AI products, they need visibility into model behavior, latency, and cost. Langfuse is becoming critical infrastructure for AI teams.

10. Replit (+408%)

The online IDE and code collaboration platform is growing fast, likely due to AI-assisted coding features and the shift to browser-based development environments.

What These Growth Rates Actually Mean

A +2000% growth rate sounds crazy, but context matters. When a tool goes from $500 to $10,000 in annual spend across all buyers, that's a 20x growth. It could mean 20 new companies at $500, or 2 large companies at $5,000. The growth rate is real, but the absolute spending base might be smaller than it appears.

However, the pattern across these 15 tools is unmistakable: companies are allocating real budget to new, AI-first infrastructure. This isn't experimental spending. It's production spending.

The Emerging Themes

AI infrastructure (LLMs, routers, embeddings): Claude, Anthropic, OpenRouter are the clear winners. Companies are standardizing on certain models and adding routing layers on top to avoid vendor lock-in. Claude's growth at +1728% reflects Anthropic's technical differentiation and customer trust.

AI data prep: Firecrawl and similar tools are growing because LLMs need clean input. The data pipeline is becoming a bottleneck, and companies are investing heavily to solve it.

Automation, but better: n8n's growth suggests that Zapier, despite its 37.4% adoption and $3,331 per buyer spend, is being challenged by more flexible alternatives. Companies want code-free automation that isn't locked into one vendor's vocabulary.

AI-assisted productivity: Gamma (presentations), Granola (meeting notes), and similar tools are automating the busywork that consumes 20% of knowledge worker time. These aren't replacing human judgment. They're eliminating formatting and summarization friction.

Observability for AI: Langfuse at +455% growth reflects a new requirement: as teams ship AI-powered features to production, they need to observe and monitor model behavior the way they would any other system.

Who Isn't Growing (And Why)

Notably absent from the fastest-growing list are traditional productivity tools like Slack, Asana, and Salesforce. These are mature, not declining. But they're growing at typical SaaS rates (10-20% annually) rather than the explosive 400-2000% we see in the AI-first category.

This suggests that AI is adding new spending categories rather than cannibalizing existing ones. A company doesn't use Gamma instead of PowerPoint. They use Gamma to make PowerPoint faster. These aren't replacement purchases. They're additive.

The 2026 SaaS Trajectory

If this trend continues, by end of 2026, AI-related spending could approach 35-40% of total SaaS spend. That would represent a fundamental shift in how companies allocate budget.

The winners are tools that solve specific AI problems: model access, data prep, workflow automation, observability, and human productivity amplification. The losers will be tools that ignore AI integration and assume their moat is sufficient.

For any company making SaaS decisions right now, the question isn't whether to invest in AI tools. The question is which ones to pick, and whether you're building infrastructure that plays well with AI-first workflows or just bolting AI on top of yesterday's architecture.

This analysis is based on anonymized, aggregated transaction data from Cledara's platform. All figures represent averages, percentages, and ratios. No individual company data is disclosed.