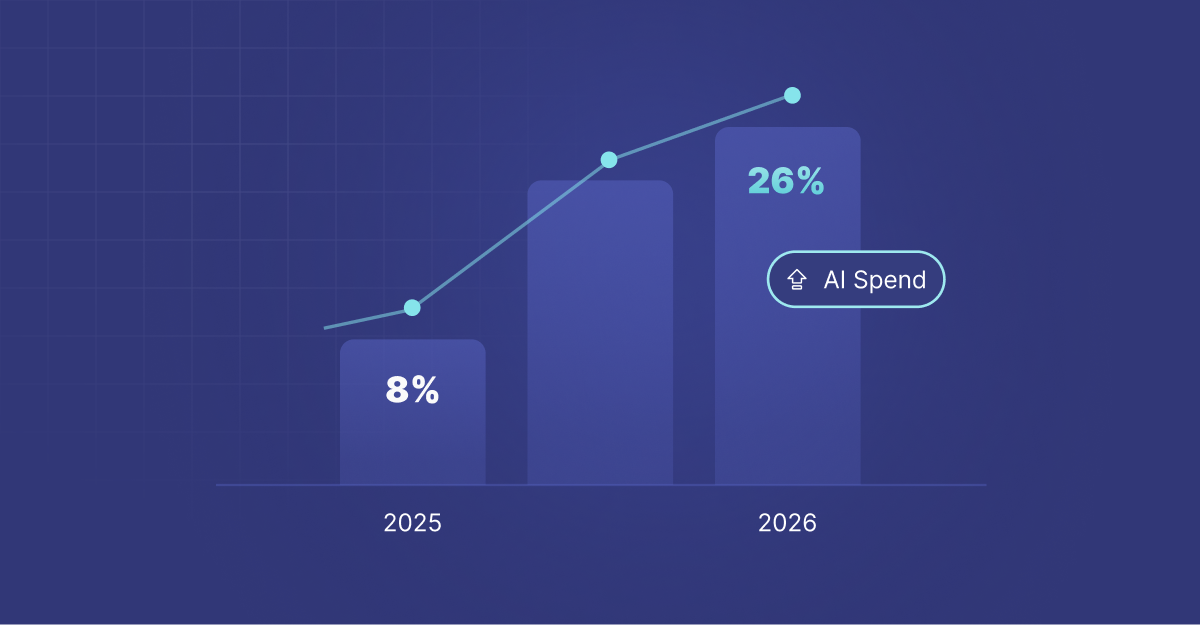

Fourteen months ago, artificial intelligence tools represented less than 9% of all SaaS transactions. Today, they represent more than one in four purchases.

The speed at which AI has rewritten the SaaS playbook is almost hard to comprehend. Traditional enterprise tools took years to reach this level of adoption. AI tools did it in months. And the momentum is far from over.

The Arc of Explosive Growth

Let's be precise about the timeline. In January 2025, AI transactions accounted for 8.8% of all purchases on Cledara. By March 2026, that number had climbed to 26.4%. That's a three-fold increase in 14 months.

What's notable isn't just the upward slope. It's the consistency of it. This isn't a spike followed by plateau. This is sustained, month-over-month growth with minimal pullback. Even as new tools enter the market and compete with each other, the overall share of AI in SaaS spending keeps climbing.

The second insight is equally important: AI tools currently represent only 5.6% of total spend, even though they account for 12.5% of all transactions. Translation: AI tools are cheaper than legacy software, yet companies are adopting them three times faster than they're cutting budget for other things.

This means AI adoption isn't replacing dollar-for-dollar spending. It's additive. Companies are adding AI tools while keeping their existing stack intact. That's a budget crisis waiting to happen for CFOs. And it's why subscription management tools like Cledara are seeing unprecedented demand.

Which AI Tools Are Actually Winning?

OpenAI, in all its forms, dominates. The company appears in roughly half of all buyer accounts. But that's not the whole story. The AI category is fractionalizing fast.

OpenAI sits at 50.4% adoption. ChatGPT (which is technically different from the platform, though from the same vendor) reaches 39.2% adoption. Claude hits 38.7%, a stunning figure given the timeline. Cursor, the AI coding assistant, sits at 30.5%. Anthropic, serving a developer-focused audience, reaches 16.5%. Midjourney, for image generation, sits at 14.1%.

But here's what's fascinating: the category is expanding, not consolidating. Grammarly for writing AI sits at 18.4%. Perplexity for AI search is at 10.6%. Lovable, a newer AI tool for building apps, is at 12.2%. Each of these tools would be a massive success if they were traditional SaaS products. In the AI landscape, they're mid-tier players.

The long tail of AI is also growing. Tools like Firecrawl (web scraping), Langfuse (LLM observability), and n8n (AI automation) have all grown more than 400% year-over-year. These aren't consumer products. They're developer-focused tools that are becoming standard infrastructure.

The Fastest-Growing Cohort: Coding and Infrastructure AI

AI coding tools are experiencing the most aggressive growth pattern of any category. GitHub Copilot, already mainstream, maintains 56.5% adoption. But the newcomers are moving faster.

Cursor, an AI-first code editor, grew from minimal adoption to 30.5% in less than two years. Windsurf, a newer competitor, is at 4.1% but accelerating. Lovable, for building AI apps, is at 12.2%. Combined, these newer tools represent the fastest wave of developer tool adoption since the cloud infrastructure boom of the 2010s.

Monthly coding tool spend tripled from January 2025 to March 2026, going from roughly $217,000 to $670,000. This isn't just adoption. It's intensity of use growing at the same time.

Why? Because software development is the first profession where AI can write production code. That changes everything. Every developer suddenly has an assistant that's faster than hiring one. The math doesn't work anymore to spend 40 hours a week on boilerplate code when AI can do it in 40 minutes.

The Displacement Game: What Are AI Tools Replacing?

This is the uncomfortable question for traditional SaaS vendors. Where is the AI growth coming from?

The data suggests that AI is carving out new spend categories rather than wholesale replacement. No traditional tool has collapsed in usage. Instead, AI tools are being layered on top, creating what we might call "stack multiplication."

But there are warning signs. For tasks like content generation, Grammarly is growing while dedicated copywriting tools are stagnant. For search and research, Perplexity is growing while traditional search tools and knowledge bases are flat. For image generation, Midjourney and similar tools are clearly eating into Adobe Creative Cloud's growth potential, though Adobe's adoption remains strong.

The pattern suggests that AI is most dangerous to tools that primarily commoditized human knowledge work. Tools that added proprietary value through human curation, training data, or specialized expertise are under pressure. Tools that solved infrastructure or workflow problems are mostly stable.

The Adoption Curve Tells a Story About Market Maturity

When you look at fastest-growing tools by year-over-year transaction growth, the names read like a who's-who of the modern AI stack: Lovable at 2,089% growth, Claude at 1,728%, Anthropic at 1,538%, Firecrawl at 1,417%, OpenRouter at 1,009%, n8n at 812%.

These aren't marginal products. These are the tools that are reshaping how work gets done. And they're not growing 1,000% by accident. They're growing because they solve problems that didn't have good solutions before.

Lovable is 2,089% growth because building simple apps used to require days or weeks. Now it takes hours. OpenRouter is 1,009% growth because companies need flexibility across multiple LLM providers. n8n is growing because automating workflows with AI requires new infrastructure.

The adoption curve for AI tools looks nothing like previous technology waves. Instead of years to reach maturity, we're seeing months. Instead of concentrated adoption among early adopters, we're seeing mainstream penetration in the first 18 months.

What This Means for Your Budget

If you're managing SaaS spend at a company right now, you're in the middle of a fundamental restructuring, whether you've acknowledged it or not.

You have teams independently signing up for Claude, ChatGPT, and Cursor, each bringing their own cost and their own licensing headaches. You have emerging AI infrastructure tools (Langfuse, Firecrawl, OpenRouter) being deployed without budget approval because they cost $50 a month and the benefit is obvious.

You have a traditional software stack that still works and still costs money. And you have new AI tools that might replace parts of it, but probably won't, because the transition cost is higher than just running both in parallel.

That's budget creep at scale. That's why companies that were spending $23.6M per quarter on SaaS two years ago are now spending $32.9M, even though they're theoretically using fewer tools (because AI is more efficient). They're not getting more done with the same money. They're getting the same amount done with more money, because they're running both stacks.

The companies that will win are those that make aggressive choices about AI adoption right now. Not whether to use AI. That's decided. But which tools, which workflows, and which legacy tools to sunset. The ones that delay that decision will find themselves managing three times as many tools in 18 months, each with its own licensing, security, and compliance headaches.

The Next Wave

If AI transaction share goes from 8.8% to 26.4% in 14 months, where is it in another 14? If coding tool spend tripled in 12 months, how much will specialized AI infrastructure grow?

The answer is probably: faster than anyone is prepared for. The vendors that will dominate the next three years aren't the ones claiming to be "AI-ready." They're the ones building for a world where 50% of all SaaS transactions are AI-native, and integration between AI tools is the new baseline expectation.

That future isn't coming. It's already here. You're just operating in the lag phase where the budget hasn't caught up with reality yet.

This analysis is based on anonymized, aggregated transaction data from Cledara's platform. All figures represent averages, percentages, and ratios. No individual company data is disclosed. For detailed market analysis, visit data.cledara.com.